Feature

Explainer: Why have there been so many job cuts in MedTech?

Since the end of the Covid-19 Pandemic multiple medical device and diagnostics firms have been cutting jobs across the industry as the post-pandemic boom winds down. By Joshua Silverwood.

Giant corporations including Johnson and Johnson, Philips and Siemens Healthineers have all seen significant workforce reductions during the first half of 2024. Credit: mkfilm / Shutterstock

Thousands of jobs across the medtech sector have been slashed by multinationals throughout the first half of this year, with research and development (R&D), diagnostic testing and North American facilities being the hardest hit as companies look to secure greater returns for investors.

Giant corporations including Johnson and Johnson (J&J), Philips, and Siemens Healthineers have all seen significant workforce reductions over the course of the first half of 2024, ranging from hundreds to thousands of staff members made redundant.

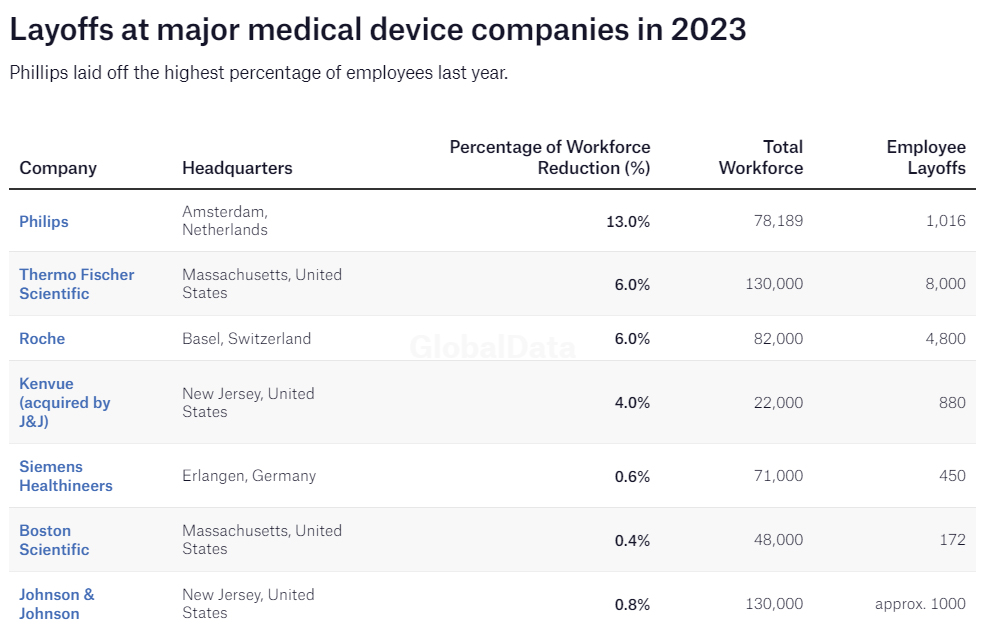

In the case of Philips, the chain of events leading to job cuts is due to a 2023 filled with recalls and quality issues, as well as an initiative to restructure itself globally in the hope of remaining profitable. In 2023, the company announced that it was cutting approximately 13% of its workforce, equating to 6,000 jobs worldwide.

Despite this, the company has seen relatively marginal savings over the year in which the cuts were enacted. In its 2022 year-end financial report, the company reported a financial loss of €1.6bn ($1.71bn). In its 2023 year-end report, the company was able to report losses of only €115m.

However, Philips has been far from alone in terms of reaping the rewards of large-scale job cuts. The layoffs come following a call from within the medtech industry itself for the EU and US to ensure companies have greater access to trained and skilled workers. To that end, Medical Device Network is examining the scale of job cuts across the industry since the Covid-19 pandemic and the seemingly contradictory calls from the industry for more skilled workers.

Source: Data from company press releases and publically available sources.

Sights on Siemens

At the annual 2024 MedTech Forum in Vienna, one of the chief talking points across multiple sessions was the impending nature of workforce sustainability in the healthcare sector, with research carried out by event hosts and industry body MedTech Europe finding that in order to maintain its current healthcare standard, by the year 2040 one in every four European workers will need to be a healthcare worker. The sentiment, echoed by many at the conference, seemingly does not apply to the similarly beleaguered US-based workforce.

In November 2023, Siemens Healthineers cut an additional 300 jobs as it sought to shutter its Healthcare Diagnostics manufacturing facility in Flanders, New Jersey. Bringing the total number of job cuts in the region up to 750 as the company looks to relocate its still existing manufacturing and R&D closer to home, namely the Republic of Ireland. The cuts come amid a drive by the company to restructure the entirety of its mostly US-based diagnostics division, with the aim of saving €300m yearly by 2025. At the time of the announcement, Siemens Healthineers stock stood at €47.97 per share; at the time of writing that stock price has risen to €53.60 per share.

Speaking with Medical Device Network at the cocktail reception of the MedTech 2024 Forum, former CEO and now senior executive for Siemens Healthineers, Martin Fuhrer, defended the job cuts arguing that they did not undermine calls for greater access to skilled healthcare staff.

Fuhrer said: “It is about having the right jobs in the right places. The job cuts that happened in Flanders come because of portfolio product decisions we made and that is it. What you need to look at is the global workforce in health. As a net, we are increasing our workforce. As a global company, you have to move people from one location to another, as a result of geopolitics and reacting to the market.”

When asked why US-based jobs had been effectively relocated to Ireland, Fuhrer detailed that the diagnostic products produced in the New Jersey facility see higher demand in the EU than they do in the US, incentivising the company to move production, especially in the wake of the supply chain disruption. Pressed as to whether such savings could be achieved without cutting on-the-ground staff, instead by reducing pay in managerial sectors or by reducing dividends to investors, Fuhrer was adamant that it was not possible.

Fuhrer added: “Do I feel sorry for them? Absolutely, yes, but we are a global company, and we need to shift products closer to the markets as a result of the Covid pandemic and supply chain disruption. If we didn’t do that, we would again run directly into logistics challenges that would lead to patients going undiagnosed or not cared for because we don’t have the right products in the right place at the right time.

These decisions are never made easy, but we have to make them.

At its annual shareholders meeting in April of this year, the current supervisory board of Siemens Healthiness approved a dividend proposal of €0.95 per share for fiscal year 2023. Usually paid out from net income, Siemens Healthineers pays out approximately 70% of its €426 net income from 2022 in dividends, representing a payout of approximately €298.2m.

Siemens is not entirely alone; the practice of reshoring supply chains has been becoming increasingly prevalent across the medtech space in the wake of the Covid-19 pandemic. In this case, Siemens is 'nearshoring' or 'friendshoring', a practice whereby supply chains are relocated to closer/friendlier countries with more agreeable trade terms. Research by GlobalData found that as many as 90% of companies involved in the practice saw positive results from the move.

Industry trends

Many of the lay-offs have their roots in the unparalleled growth the largely US-based diagnostics scene experienced as a result of the Covid-19 pandemic and its unique set of restrictions and occasional benefits that saw some areas of the health tech space benefit whilst others faltered.

One of the areas that saw significant growth for evident reasons was the in vitro diagnostics scene, with governments worldwide directly incentivising the development of more and more complex Covid-19 rapid antigen tests in the hope of curtailing the spread of the virus.

Selena Yu, healthcare analyst for GlobalData, detailed how, in the wake of the Covid-19 pandemic, many companies hoped to translate the direct investment into more varied and marketable tests off of the back of Covid-19 investment, but these hopes did not materialise, leaving diagnostics companies with over-investment in a quickly dwindling and busy market.

Yu said: “[Diagnostics companies] made a lot of money during the Covid-19 years and now, since Covid is less and less of a thing, many of these companies are writing it as a loss because they upscaled so much in terms of Covid production. Companies like Siemens put a lot of money in R&D around Covid-19 testing and now that testing is no longer as lucrative, they have back-peddled and tried to make some of their tests multi-panel or more accessible. They tried to use that money put into R&D and rebrand these tests as new kinds of tests, and from what we can see that has not been very successful.”

Yu detailed how throughout the Covid-19 era the US diagnostics space found itself quickly taken over by giant corporations such as Roche or Abbot, which already had significant dominance in the market prior to the pandemic. However, with large investments being made into the diagnostics market driven sharply upward by an increased demand for testing, many smaller medtech companies similarly looked to get involved in a market that was quickly appearing saturated in hopes of a quick turnaround.

Yu added: “Smaller companies, where many other lay-offs are also coming from, would look to develop their own Covid-19 tests and end up getting acquired by these giant companies, which then look to dissolve them. For the US there are emergency authorisations of Covid tests still coming through today. This, I think, goes to show just how much money these companies put into Covid-19 testing during the height of the pandemic.”

As the economic boom experienced by the diagnostics industry begins to dwindle as the Covid-19 pandemic fades into popular memory, so too will much of that boom-era investment. This means that while many companies may continue to try to push their overstretched diagnostics wings to become profitable, it is likely that further job cuts and redundancies will follow as they begin to realise that the industry has moved on.

The mine’s concentrator can produce around 240,000 tonnes of ore, including around 26,500 tonnes of rare earth oxides.

Gavin John Lockyer, CEO of Arafura Resources

Total annual production

Caption. Credit:

Phillip Day. Credit: Scotgold Resources